Understanding trends in the expanding protein market from a consumer needs perspective

A variety of consumer needs have emerged since our lifestyles were impacted by the spread of covid-19 in 2020 onwards. A wide range of markets have benefited from booming demand for ways to enhance base-line physical wellness and immunity to prevent covid infection, as well as ways to enrich time spent at home.

The protein market is one such case. While protein powder has enjoyed growth mainly among seniors as a means to prevent frailty since pre covid times, it has continued to grow thanks to the winning over of young women concerned about physical activity and diet due to covid.

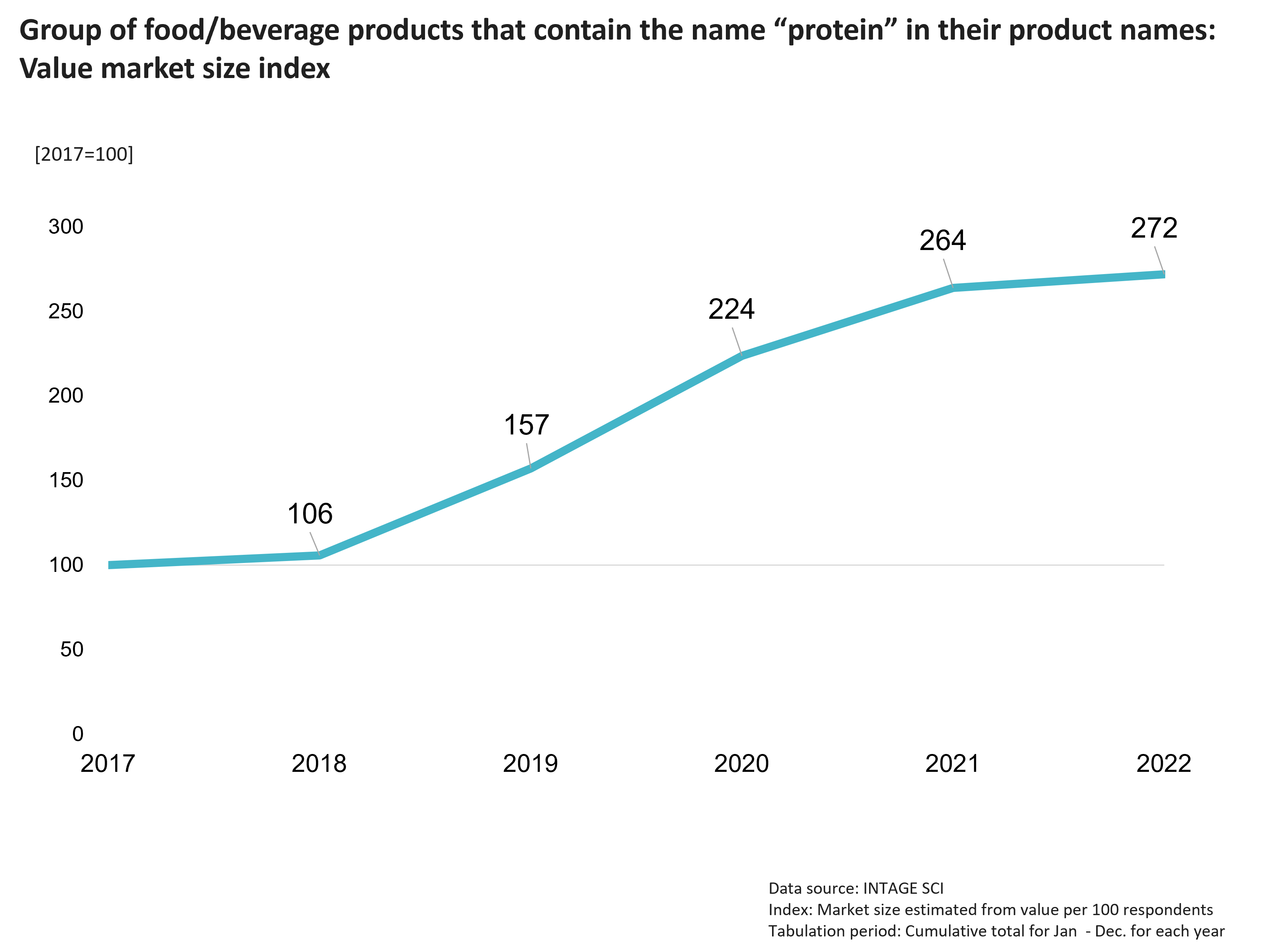

There are now also a variety of food products and beverages that contain protein, which now make up a broad “protein market”. We examined shifts in the protein market’s monetary market scale via INTAGE SCI (*1) data by defining the market as the group of food products and beverages that carry the name “protein” in their product names (See Fig.1)

Fig.1

If we set the market’s size to 100 in 2017, it rapidly climbed to 157 in 2019, when instant-type protein beverages and bar-type food products were released from a range of firms. It then reached 272 in 2022 following ongoing growth through the covid crisis.

The release of a variety of protein products is assumed to drive not only increases in the number of users, but also the diversification of their needs and consumption occasions. This article will thus explore the protein market from a consumer needs perspective, and examine current market trends.

“Shopping Log WOM Data ” from the shopping app “CODE” was used in our analysis. This data is entered when purchasers register the products they purchase in app. It mainly describes the reasons why they go on to purchase those products, such as their purpose, and in what sorts of situations or occasions they intend to use/consume it in.

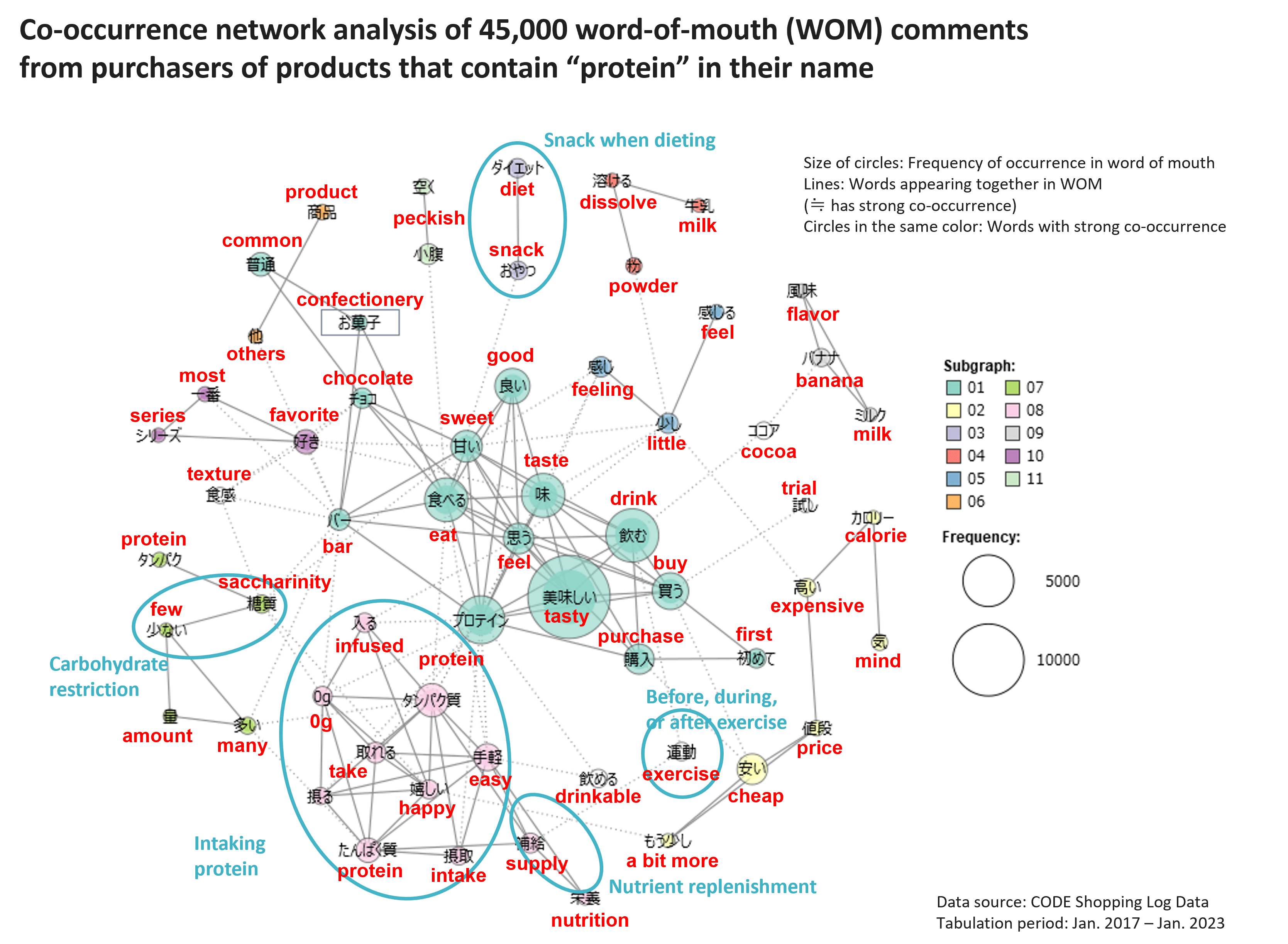

We next conducted a co-occurrence network analysis (*3) on approximately 45,000 WOM reviews by purchasers of products and services that carry the word “protein” in their name, as seen in Fig.2. On examination of the sorts of consumer needs that were included within the reasons for protein product purchase in this Fig.2, it became apparent consumers have needs including “cutting back on sugar”, “intaking nutrients”, and “intaking protein”. It was also apparent such products are also purchased with consumption “as a snack when dieting” or in “pre, mid, and post exercise” situations in mind.(Universal needs associated with food products and beverages such as “delicious” and “sweet” were excluded from the scope of our analysis)

Fig.2

While its relationship with the other keywords is weak, and thus cannot be depicted in this Fig.2, “weight training” is another situation that must be kept in mind. It occurred quite frequently.

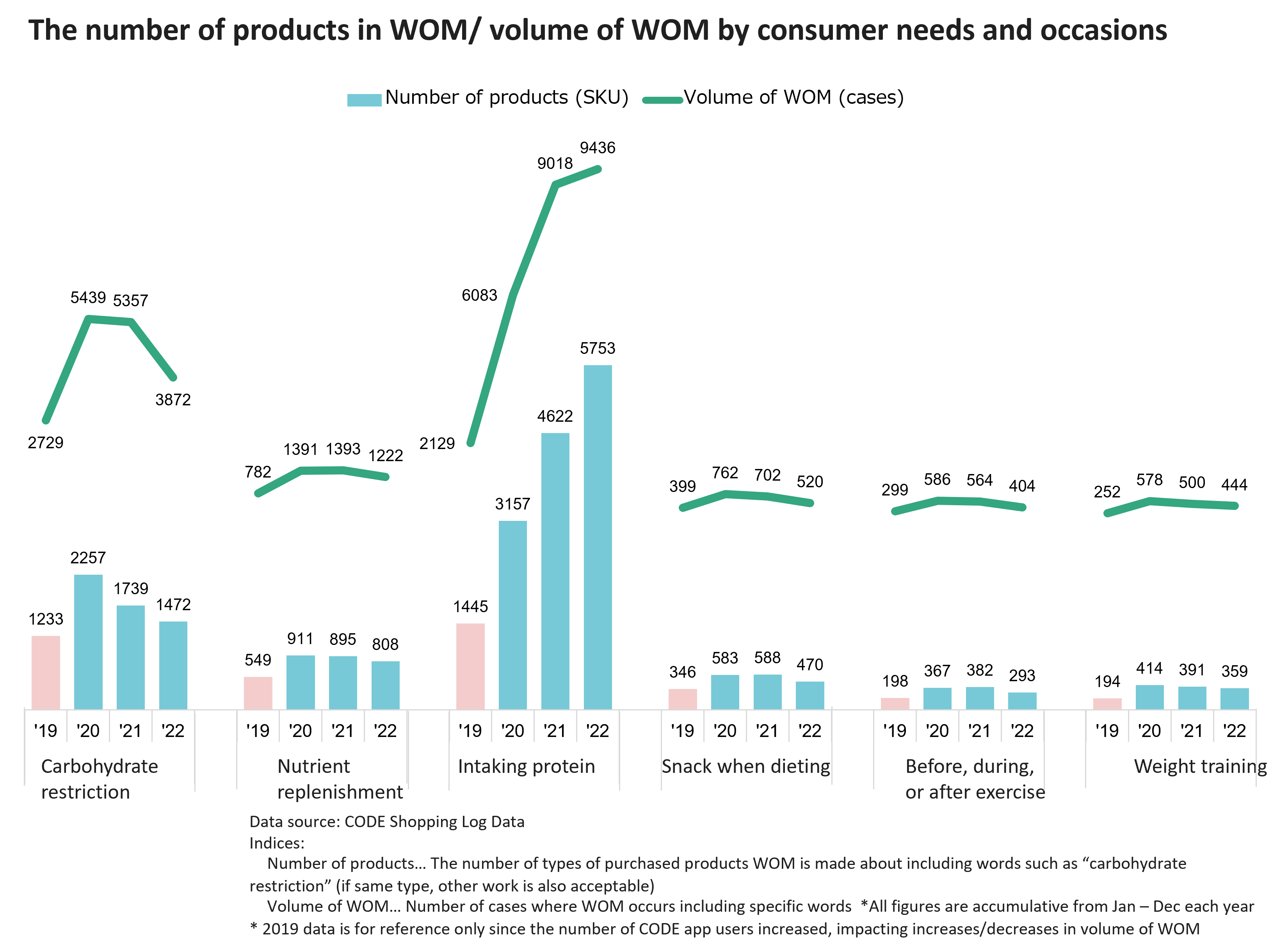

To examine whether demand driven by these sorts of needs and situations is on the increase year by year, we examined shifts in the number of WOM reviews including each keyword, and number of products WOM reviews have been given for over time. (Here, all products WOM reviews were given for comprise the scope of target, not just protein products.) (Fig.3)

Fig.3

“Intaking protein”, in first place in terms of number of WOM reviews and number of products that WOM reviews were given for, rapidly increased from 2020 to 2021 amidst the covid crisis in line with the increase in health consciousness. Protein is a key nutrient to build a healthy body and extend healthy life expectancy with among all age groups, so demand is expected to remain stable/grow in future.

On the other hand, “carb restriction” peaked in 2020, and is now on a downward trend. This is indicative of the fact that since the advent of covid, consumers are no longer interested in outlooks on health focused on “restriction”, but instead are interested in outlooks focused on weight training/exercise + “intaking” protein.

In addition, on observation of the objectives “intaking nutrients” and “snacks when dieting”, and the situations “pre, mid, and post exercise” and “weight training”, the greatest number of WOM reviews/number of products were observed in 2020 ~ 2021. The rise in demand for dieting and exercise to alleviate “covid weight gain” that has occurred during stay home periods appears to have settled once consumers returned to their daily lives.

Competitors to protein products from a consumer need and situational perspective

So, what sorts of products other than protein are used for the aforementioned needs and situations? Clarifying this may offer hints regarding potential new directions to develop the category along. From this point onwards, we thus examined the sorts of products consumers purchase for each of these needs and situations. Note that similar keywords expressing needs and situations are also included in the scope of tabulation.

① Carb restriction

If we set the number of WOM reviews including the keyword “carb restriction” to 100%, the top three categories were beers (approx. 16%), sweets (10%), and confectionary/fancy bread (9%). Beers received WOM reviews from reduced carb and zero carb type purchasers. While ranking 1st even before the covid crisis, it increased its share even further due to drinking-at-home demand along with heightened health consciousness during the covid crisis.

Second-place sweets received WOM reviews for a variety of products, including reduced sugar eclairs, cream puffs, cakes, and donuts. Third-place confectionary/fancy bread received WOM reviews for reduced carb products mainly offered by the various CVS chain firms.

At the same time, while WOM reviews were given for protein products like protein bars, these were only given by a very small few.

These findings indicate that there is a strong need for carb restriction in categories that are more items of preference and are normally quite high carb. The motivation to cut back on carbs by replacing these products with protein products is likely to be weak, since the issue here is how carbs can be cut back on with foods consumers are already accustomed to eating/drinking.

➁ Intaking nutrients

If we set the number of WOM reviews including the keyword “intaking nutrients” to 100%, the top three categories were sports drinks (23%), nutritionally balanced food products (11%), and nutritional drinks (7%).

The top products comprising first-place sports drinks were jelly-type energy replenishment and vitamin/mineral replenishment beverages, with this category well established for nutrient intake purposes.

Protein products received WOM reviews for sports drinks containing jelly-type protein and protein bars. However, only a very small number of WOM reviews were received for them, indicating that consumers still do not strongly connect intaking nutrients with intaking protein.

③ Intaking protein

If we set the number of WOM reviews including the keyword “intaking protein” to 100%, the top three categories were chicken meat (9%), yoghurt (8%), and nutritionally balanced food products (6%).

First-place chicken meat received the most WOM reviews, led by breast meat purchasers. Second-place yoghurt mainly received WOM reviews on products laying claim to protein contents, and third-place nutritionally balanced food products to protein bars and milk beverages that contain protein.

Ingredients and food products that are easily incorporated into one’s daily diet rank top, with protein products also well-established among these products.

While the number of products receiving WOM reviews as enabling consumers to “intake protein” has increased year by year, there are ever increasing options for consumers, so there is an increasing risk of being replaced by competing products or competing categories.

④ Snacks when dieting

If we set the number of WOM reviews including the keywords “snacks when dieting” to 100%, the top three categories were savory snacks (18%), desserts (13%), and nutritionally balanced food products (7%). Savory snacks mainly received WOM reviews for chewing kelp, dried squid, and nuts such as almonds, while desserts were mainly konjac-type jelly and low carb type products. In addition, compared to pre covid times, the number of WOM reviews for high cacao content chocolate, salad chicken, and high protein yoghurt has increased. In diet situations, there seems to be a change in outlook, with consumers wanting not only to restrict carbs, but to supplement nutrients at the same time as well.

Limited WOM reviews were received for protein-related products, indicating they may be positioned instead of being snacks≒ something to satisfy a light hunger with, as being closer to a meal≒ something one goes to the trouble of eating. However, protein products may take root in snack situations as well depending on the products deployed and their communication in future.

⑤ Pre, mid, and post exercise

If we set the number of WOM reviews including the keywords “pre, mid, and post exercise” to100%, the top three categories were sports drinks (28%), dairy beverages (15%), and nutritionally balanced food products (approx. 6%). Sports drinks have a firmly established position. Dairy beverages mainly received WOM reviews for protein beverage and low-fat milk, and nutritionally balanced food products mainly protein bars.

Increased health consciousness and a need to alleviate physical inactivity during the covid crisis may have increasingly established the position of “protein” for physique building and fitness training, rather than for mere exercise

⑥ Weight training

If we set the number of WOM reviews containing the keywords “weight training” to 100%, the top three categories were chicken meat (approx. 27%), dairy beverages (approx. 11%), and nutritionally balanced food products (approx. 7%).

By far the most WOM reviews for chicken meat were for breast meat. While fillets are low fat and healthy, so seem likely to be favored at a glance, breast meat appears more accepted due to its cheapness per gram generally in store.

The top dairy beverages were protein-type beverages, which are available in a variety of flavors and sizes, while the top nutritionally balanced food products were the protein bars offered by a variety of manufacturers. Consumers are clearly now of the perception that one “intakes protein when engaging in weight training”. However, as individuals differ in the extent to which they engage in this, protein products that can be easily incorporated into one’s daily dietary lifestyle seem more likely to be accepted.

The importance of understanding the market from a consumer need and situational perspective

The fact consumers select protein products from a variety of options depending on their needs, objectives, and situations is clear from this study’s analysis. For example, we identified that with “snacks when dieting”, protein products are potential substitutes for savory snacks and desserts, indicating they may be a potential share source for protein products.

Adopting a different perspective to see things from a broad consumer perspective, rather than merely observing the market and relationships with competitors from a category perspective should provide hints with which to win over new customers.

*1 SCI® (nationwide consumer panel survey) A nationwide individual consumer panel survey continuously gathering the daily food product (including perishables, pre-cooked dishes, bento boxes etc.), beverage, daily sundries, and pharmaceuticals shopping from 53,600 male and female 15 ~ 79-year-old consumers nationwide.

*2 Research and Innovation CODE Shopping Log WOM reviews entered by users of “CODE”, a shopping app offered by Research and Innovation on the items they purchase. CODE has accumulated approx. 59 million WOM reviews linked to actual purchases and approx. 97 million evaluation reviews by approximately 300,000 MAUs (users who use it once a month or more).

*3 A type of co-occurrence network analysis text mining tat visualizes the connections between words in statements, based on the similarity of relationships between words and their occurrence patterns. This enables us to identify characteristics in large volumes of text data, such as WOM review data, questionnaire open-end responses, and newspaper articles. Source: Tokyo University of Science https://www.tus.ac.jp/today/archive/20220411_3957.html

This article is based on the results of a self-directed survey conducted as part of priority initiatives by INTAGE’s Customer Business Drive Headquarters and Business Development Headquarters.

(Written by Hiroyuki Tanabe, with editorial assistance from Ai Horikiri, Kazuki Miyaji, and Daiki Meguro, written by Hiroyuki Tanabe)

Reproduction and Quotation

◆This report is copyrighted by INTAGE Inc. Please check the following prohibitions and precautions, and specify the source when reproducing or quoting this report. “Source: INTAGE “Knowledge Gallery” article published MM/DD/YYYY article”

◆The following are prohibited: ・Alteration of this article in full or in part ・Sale or publication of this article in full or in part ・Uses that are against public order and morality, and uses connected with illegal activities ・Reproducing or quoting panel data* for the purpose of advertising or promoting companies, products, or services *Panel data include: SRI+, SCI, SLI, Kitchen Diary, Car-kit, MAT-kit, Media Gauge, i-SSP, etc.

◆Other precautions: ・INTAGE Inc. shall not be liable for any trouble, loss, or damage caused by the use of this report ・These usage rules do not restrict the use of quotations or other uses permitted under the Copyright Act of Japan

◆For inquiries about reproduction and quotation, click here.