Consumer shopping behavior post covid – Changes seen via shopping app data

Since covid shifted to a class 5 infection in May 2023, prohibitions on a variety of events have been lifted, consciousness regarding the infection has declined sizably, and life is increasingly returning to normal. At the same time, some of the changes to our lifestyle brought about by the covid crisis, such as how we interact with others and remote work, have actually taken hold. It appears that the prediction made by some experts at the beginning of the covid crisis that “even after the covid crisis ends, the landscape won’t completely return to normal” has gone on to be true.

One of the sizable changes it has brought about with consumer post covid has been an increased burden on household budgets. 2023 in particular can be said to have been a year where consumer consciousness of protecting their lifestyles increased greatly, due to concerns about the increasing prices of a plethora of goods and services sparked by the soaring prices of crude oil and other raw materials from the previous year, along with concerns about the future such as increased taxes and an increased social insurance burden.

These changes in awareness have brought about sizable changes in consumer shopping behavior. This article will thus examine changes in shopping behavior post covid, along with hints for how the retail sector who supports this shopping can respond to these changes from big data accumulated via shopping app data.

The shrinking trading areas of retail stores accelerated by the covid crisis

The area from which a store expects consumer to visit is referred to as its trading area. Trading areas are defined in different ways depending on the channel and company, such as by the “distance from store”, or “area where customers who account for xx% of sales live”. In recent years, these trading areas are said to have been getting smaller, with this phenomenon known as the “shrinking of trading areas”. The shrinking of trading areas is caused by long-term, gradual changes including population decline, an increase in the proportion of senior citizens, over saturation of stores in a given area, and the popularization of e-commerce. However, there have also been rapid changes to our lifestyles brought on by covid of late – the short-term, rapid shrinking of trading areas. And these rapid changes are also apparent in the data.

“CODE”, a shopping app run by Research and Innovation Inc., part of the INTAGE Group, has 300,000 users registering their shopping on app every month. This shopping data also allows us to approximate the rough distance from a user’s home to store from the postal code the user registers and the address of the store at which they have shopped. We used this estimated distance to analyze how shopping has changed.

Note that the way consumer get around transportation-wise, and the range of their daily activities differs depending on the area, such as whether they live in an urban or rural area, making it hard to analyze trading areas across the board nationwide, so our analysis this time focuses on Tokyo and neighboring Kanagawa, Saitama, and Chiba prefectures.

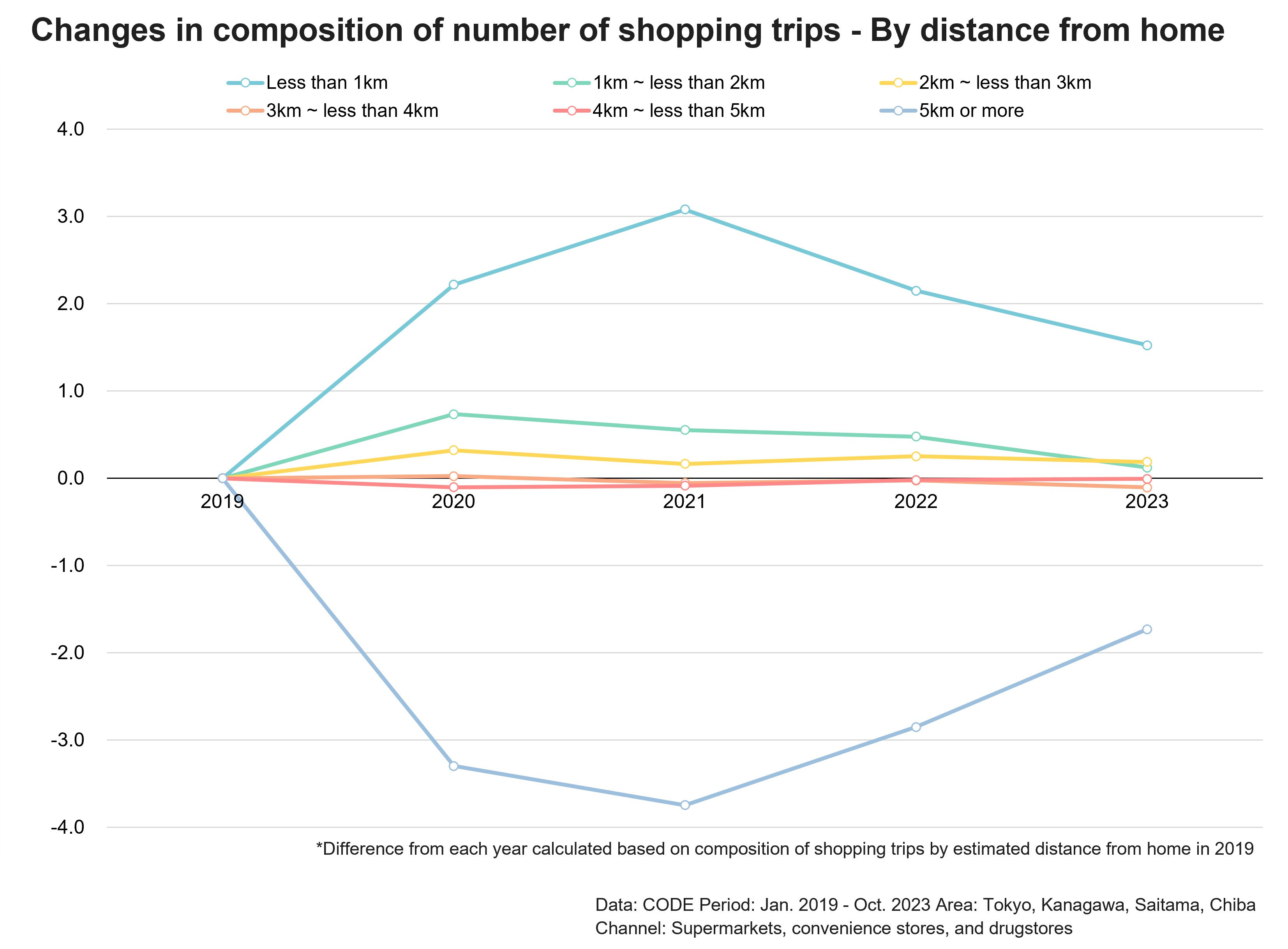

Fig 1 is a graph that calculates the number of shopping trips by distance from home to store with supermarket, convenience store, and drugstore shopping, and depicts changes in the composition of this. Let’s take a look at how things have changed since pre covid 2019.

Fig 1

From 2019 to 2021, the composition of “shopping nearby” less than 1km from home increased, while “shopping far away/when out” 5km or more from home decreased. This is deemed due to consumer having fewer opportunities to use stores far from home, and having more opportunities to use stores near their homes due to the increase in telework and decrease in travel/leisure caused by Japan residents’ self-restraint in staying home during the covid crisis. That is, the changes in the environment brought on by the covid crisis rapidly accelerated the shrinking of trading areas. Since 2022, we are gradually returning to 2019 levels due to the relaxation of self-restraint in staying home, although even in 2023, with covid now treated as a class 5 infection, we are still not all the way back. Changes to our lifestyles brought about by covid are deemed to even today be impacting our shopping.

On closer examination of this graph, it is also apparent that “the distance that clearly divided increased or decreased shopping opportunities during the covid crisis was 3km”. That is, broadly speaking, shopping opportunities at less than 3km increased, yet at 3km or more decreased. We’ll examine how the nature of shopping changed with both “shopping at less than 3km” and “shopping at 3km or more” in the next section.

Changes in shopping location by distance and channel

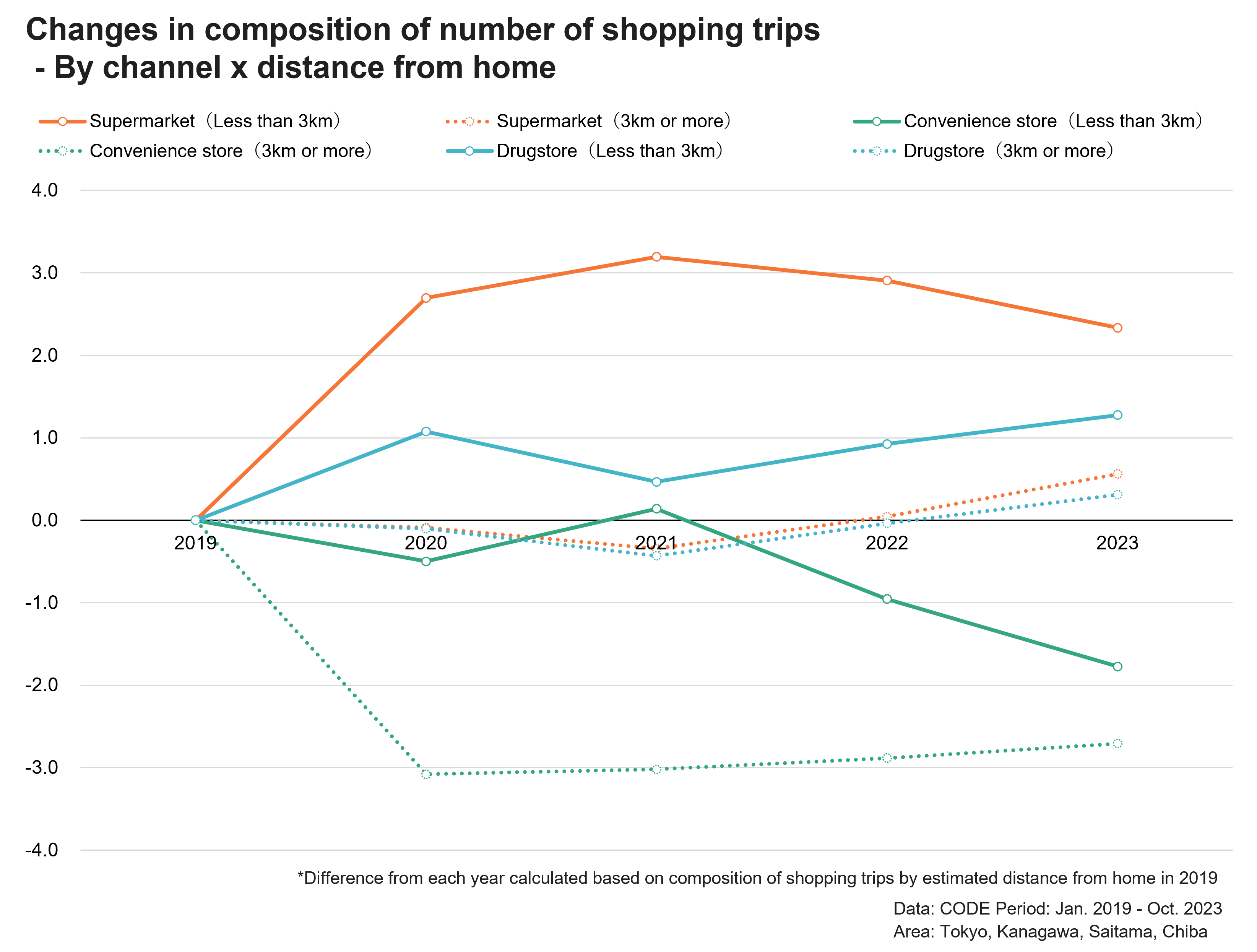

Fig 2 dissects Fig 1 from a moment ago into the 3 channel of supermarkets, convenience stores, and drugstores.

Fig 2

Assuming that less than 3km “is near home” and that 3km or more is “far from home”, supermarkets near home have increased their composition the most compared to before the covid crisis. The channel that decreased its composition the most was conversely convenience stores far from home. That is, the covid crisis changed the places consumer shop at across distances and channel from “convenience stores far from home” to “supermarkets nearby”. Another point of note is that supermarkets and drugstores near home have increased their composition, while convenience stores near home have decreased their composition for the past 2 years. That is, composition has not increased equally across all channel, indicative of the fact that the channel consumer use has changed even with stores near home. Fig 3 further dissects Fig 2 into gender.

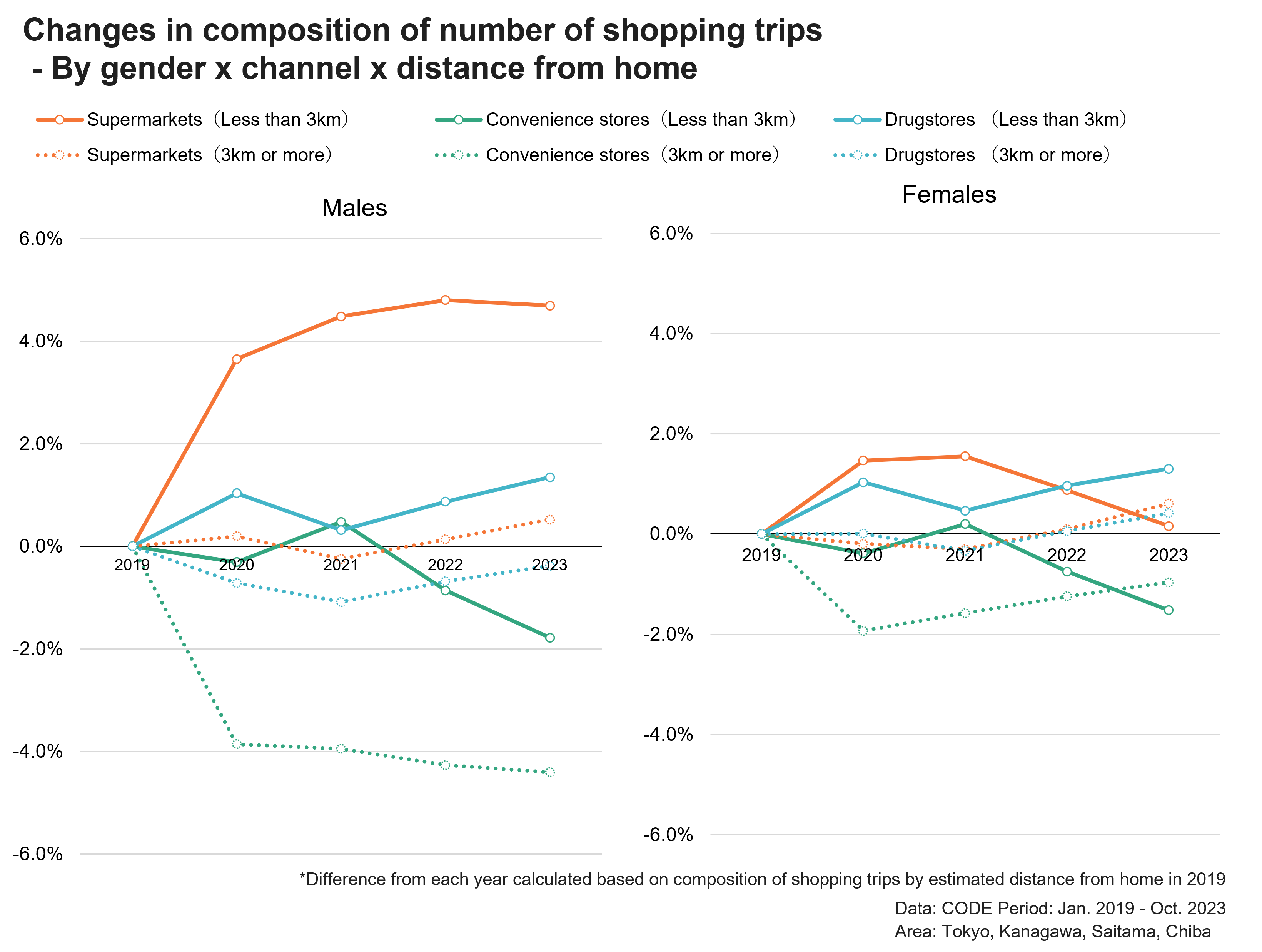

Fig 3

Firstly, the composition of supermarkets less than 3km away sizably increased, while the composition of convenience stores 3km or more away sizably decreased among males. These changes continued in 2023. Similarly, the composition of supermarkets less than 3km away increased, and the composition of convenience stores 3km or more away decreased among females in 2020 and 2021. However, there is less of a disparity between increases and decreases than among males, and by 2023, it returned to levels not much different to 2019. In other words, this shift in shopping behavior from “far away convenience stores” to “nearby supermarkets” occurred more in males than females.

What is behind these changes in shopping behavior?

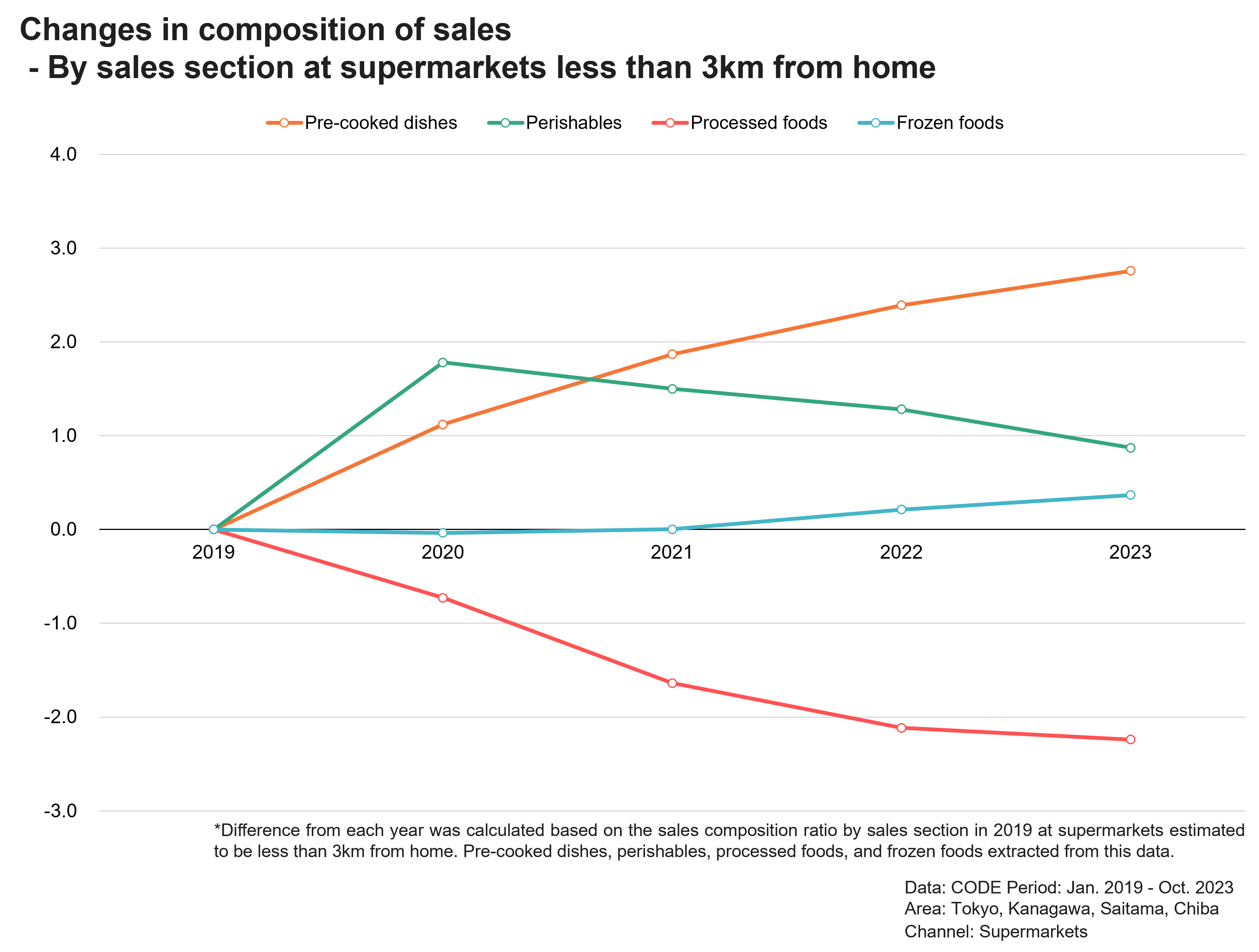

What is behind these changes in consumer shopping behavior? Let’s examine the drivers to these changes from the sales sections consumer use. Fig 4 depicts the changes in sales composition by sales section at supermarkets less than 3km away from home.

Fig 4

When the covid crisis began in earnest in 2020, the state of emergency declaration led to a rise in people refraining from going out and engaging in remote work, in turn leading to an increase in the proportion of people working from home and in leisure time. As a result, meals that were previously eaten when out were replaced by meals at home, and the sales share of perishable food and pre-cooked dishes increased. In 2021 the following year, as the practice of refraining from going out gradually weakened, people also increasingly went out due to “covid fatigue”, spent less leisure time at home, and the time they spent on cooking also decreased. Amidst this status quo, perishable food’s share decreased, while the share of pre-cooked dishes that don’t take time to cook increased.

Pre-cooked dishes continued to increase its share in the 2 years after that (2022 and 2023) as well. In the last two years, there have been a plethora of price increases by various manufacturers due to the soaring prices of crude oil and base ingredients, leading to an increased awareness of economizing. There are thus deemed to now be more opportunities to purchase fuss-free cheap, tasty pre-cooked dishes. Similarly, the increase in the share of frozen foods and decrease in the share of convenience stores, which are more expensive than supermarkets, are due to decreased cooking time and an increased awareness of economizing.

In other words, the change in consumer shopping behavior since the advent of the covid crisis is deemed due to changes in their lifestyles and outlooks, such as increases/decreases in their cooking time at home, as well as increased consciousness of getting the most out of their time and money.

We have examined the changes in consumer shopping behavior since the advent of the covid crisis through data accumulated by our shopping app. In the next section, we’ll examine these changes from the perspective of the retail stores that engage with consumer shopping.

Trend for competition within trading areas to intensify

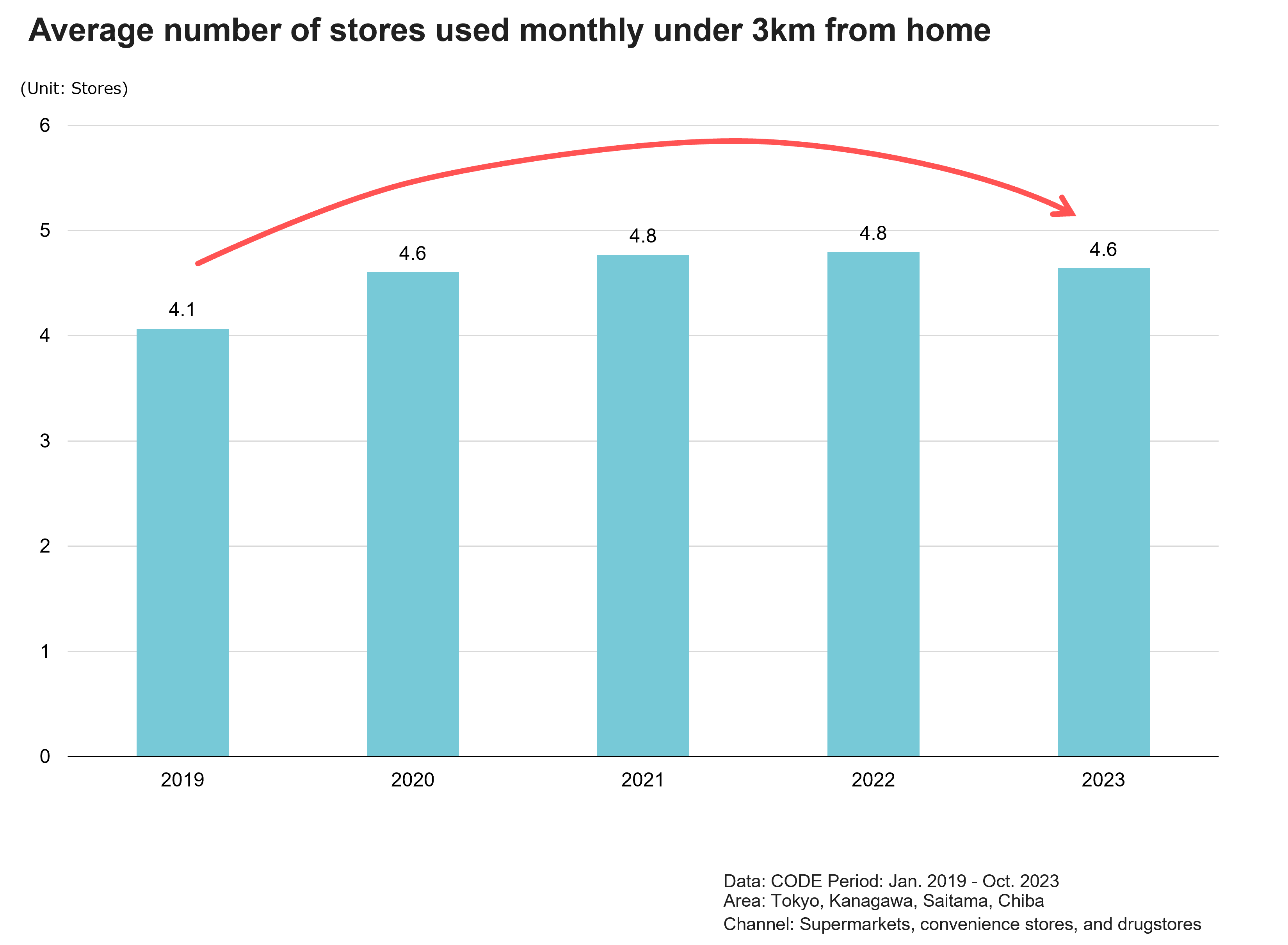

How have changes in consumer shopping behavior since the advent of the covid crisis affected competition among retail stores? Fig 5 depicts how the average number of stores (supermarkets, convenience stores, and drugstores) used under 3km from consumer homes has shifted.

Fig 5

While consumer used 4.1 stores per month on average pre covid, this increased at the advent of the covid crisis to 4.8 stores in 2021. However, this number did not increase after this, and decreased to 4.6 stores in 2023. On observation of the number of stores released by industry groups etc. for 2023, while the number of convenience stores has slightly decreased, the number of supermarkets and drugstores has increased, with the number of retail stores thus not appearing to have changed sizably overall. Taking the fact the number of stores consumer use is decreasing, competition within trading areas is deemed to have picked up in 2023.

On observation of the number of stores used at 4.6 stores a month on average by channel, the average is just under 2 stores for supermarkets and convenience stores, and just over 1 store for drugstores. Supermarkets and convenience stores may thus need to be in the top 2 stores in the area, and drugstores may need to be the top store in the area to become established in that area.

Grasping changes in consumer and creating stores that get chosen

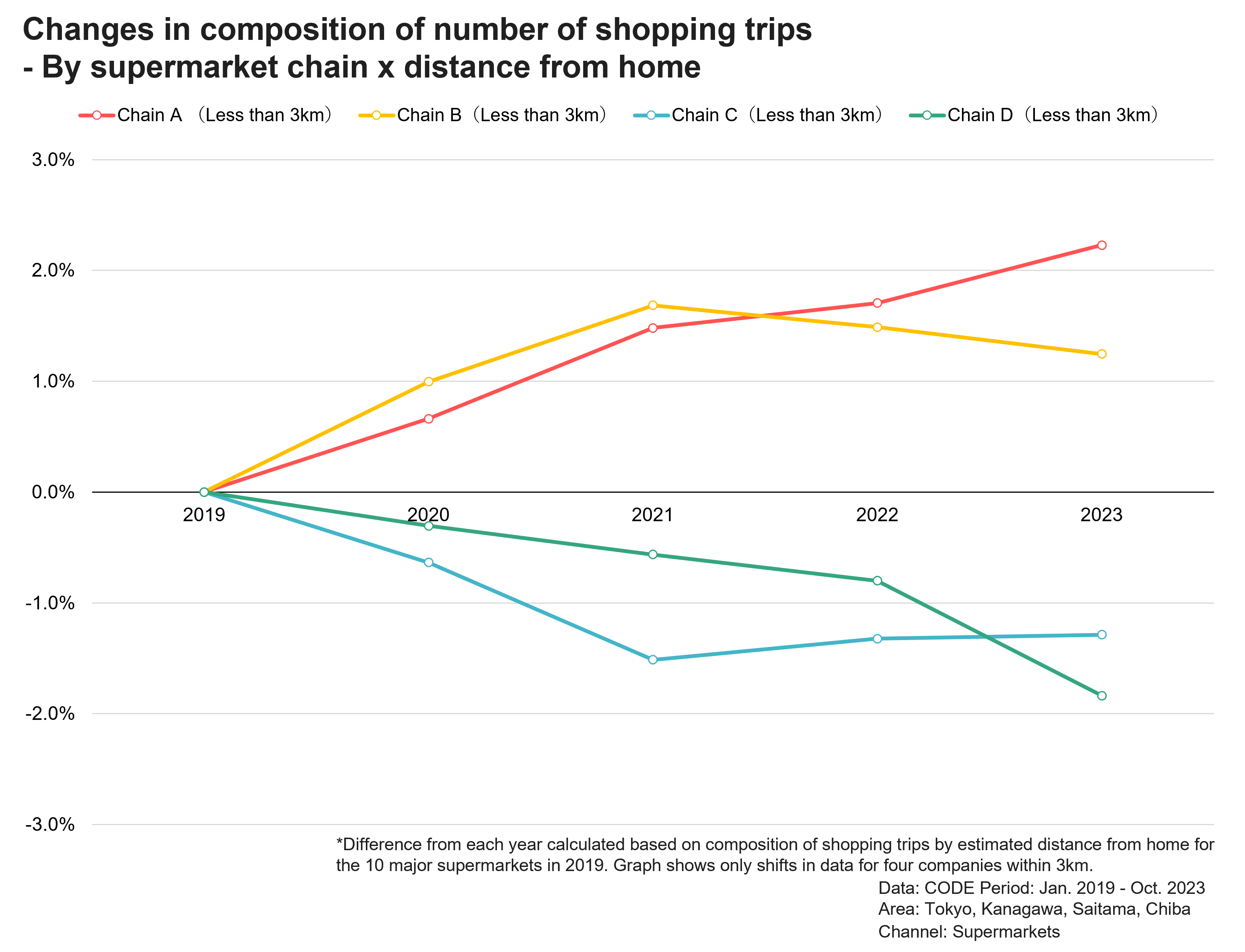

Fig 6 depicts changes in composition in the number of shopping trips at 10 leading supermarket chains in the Tokyo metropolitan area by distance from home, focusing only on data for the 4 chains under 3km from homes.

Fig 6

Among the stores less than 3km from home, Chain A has continued to increase its share since when the covid crisis began in earnest in 2020. Chain B conversely increased its share until 2021, then has tended to decline over the past 2 years. It benefitted from the special demand generated by the covid crisis until 2021, but does not appear to have been able to successfully respond to changes after then. Chain D decreased its share yearly since the start of the covid crisis, with this downward trend intensifying since 2023.

Just as the change in share of number of shopping trips since the advent of the covid crisis has not been the same across the board for all channel, it is clear that even within supermarkets near home, the performance varies by chain as well. In addition, on observation of the characteristics of chains increasing their share on the number of shopping trips, virtually all of them are chains offering EDLP (Everyday Low Prices) and pre-cooked dishes and can be said to be chains that offer stores suited to consumer heightened consciousness of getting the most out of their time and money.

Consumer outlooks and shopping behavior related to the retail sector are in a constant state of flux. Retailers are also changing in various ways to respond to this, including reviewing their operation methods, promoting DX, and leveraging AI. In order for retailers to survive in this era of sizable change for both sellers and buyers, it will be important to observe changes in consumer shopping behavior in general within trading areas beyond individual channel in a timely manner, ascertain the changes in outlook driving this, and to aim at offering stores that customers will choose to shop at.

Author profile

Masashi Nishida

Deputy Director, New Business Department, Research and Innovation Inc.

Nishida joined Transcosmos in 2000, and has worked for financial institutions, market research firms, and publishers before commencing his current role in 2023. In his career to date, he has engaged in a variety of data-related “data-based profit improvement” projects from a consulting and research perspective.

Deputy Director, New Business Department, Research and Innovation Inc.

Nishida joined Transcosmos in 2000, and has worked for financial institutions, market research firms, and publishers before commencing his current role in 2023. In his career to date, he has engaged in a variety of data-related “data-based profit improvement” projects from a consulting and research perspective.

Reproduction and Quotation

◆This report is copyrighted by INTAGE Inc. Please check the following prohibitions and precautions, and specify the source when reproducing or quoting this report. “Source: INTAGE “Knowledge Gallery” article published MM/DD/YYYY article”

◆The following are prohibited: ・Alteration of this article in full or in part ・Sale or publication of this article in full or in part ・Uses that are against public order and morality, and uses connected with illegal activities ・Reproducing or quoting panel data* for the purpose of advertising or promoting companies, products, or services *Panel data include: SRI+, SCI, SLI, Kitchen Diary, Car-kit, MAT-kit, Media Gauge, i-SSP, etc.

◆Other precautions: ・INTAGE Inc. shall not be liable for any trouble, loss, or damage caused by the use of this report ・These usage rules do not restrict the use of quotations or other uses permitted under the Copyright Act of Japan

◆For inquiries about reproduction and quotation, click here